required minimum distributions could push you into higher taxes")

I get investments wrong all the time. Losing money is part of the game.

But after I FIRE’d in 2012, the math changed. With no paycheck to bail me out, I could no longer afford big mistakes.

This post will help you think about life after FIRE, and share why it’s critical to stay measured through all the hype, do your own due diligence, and stop blindly following highly paid financial pundits.

The Joy Of Being A Wall Street Strategist

One of the cushiest jobs you can land out of college is Wall Street strategist. I worked alongside them for 13 years at two firms. They wrote in-depth research reports and met with institutional clients around the world. Smart people, well-meaning people. And often spectacularly wrong.

As I climbed from grunt analyst to Associate to VP to Director at Goldman Sachs and Credit Suisse, the thing that amazed me most was how sticky their jobs were. They could be wrong like Donkey Kong and still keep their seats. Better yet, many were Managing Directors pulling at least $400,000 in base and $600,000 or more in bonus, for total comp north of $1 million.

Here I was, hitting a bamboo ceiling while doing right by my clients. There they were, climbing to the top while blowing call after call. The higher you go, the more the meritocracy breaks down, and the more who-you-know and office politics take over. Naturally, they all felt they’d earned every dollar.

So around 2009, when I decided the system was broken and I wanted out, I stopped being lazy and launched Financial Samurai. Instead of complaining that the world isn’t fair, I figured I’d go build my own meritocracy.

No Salary. No Safety Net. Excuses Don’t Matter.

When you leave a steady job to pursue financial independence (FIRE), something fundamental changes in how you relate to your investments. They are no longer abstract numbers on a screen. They are your income, your healthcare, your kids’ education, your retirement, and your peace of mind, all rolled into one portfolio.

Ah, no wonder why it’s so hard to convince anybody to FIRE in real life!

Wall Street strategists make forecasts with little-to-no skin in the game. If they are wrong, they collect their bonus anyway, update their models, and appear on CNBC the following week with a new target.

Their lifestyle does not change based on their calls. Their mortgage gets paid regardless. This creates a very particular kind of intellectual freedom, the freedom to be confidently wrong at scale, with few personal consequences.

When you are managing your own money in FIRE, none of that applies. You watch your portfolio more carefully not so much because you are paranoid, but because the feedback loop is direct and immediate. A 30% drawdown is not a quarterly talking point. It is a question of whether you or your spouse need to go back to work or at least start more side hustles.

Having real skin in the game makes you a more honest, more disciplined investor. You cannot afford to hide behind narrative. You have to own your decisions, update your thinking when you are wrong, and stay directionally positioned for long-term growth without taking risks that could permanently impair your lifestyle.

A Useful Illustration: A Wall Street Strategist’s Calls

Mike Wilson, Morgan Stanley’s chief U.S. equity strategist and CIO, is a good illustration of what it looks like when there are no consequences for being wrong.

Wilson is smart and articulate, and I do not doubt his sincerity. But his track record over the past seven years shows what happens when a person can keep their job, their platform, and their paycheck regardless of outcomes.

In 2019, Wilson set his year-end target at 2,750, calling for essentially flat markets. The S&P 500 finished at 3,231, up nearly 29%. Missing out on 29% gains is massive. At a 4% safe withdrawal rate in FIRE, that is over 7 years of lost coverage.

In 2020 he remained cautious with a target ceiling around 3,000. The index ended at 3,756, up 16%, even after a pandemic crash briefly vindicated his caution before the Fed intervened spectacularly. That is another 20%+ miss.

In 2021 he called for a meaningful correction back toward 4,000. Instead the market marched to 4,766, up 27%. That’s three years in a row of badly off calls. If you had shorted the S&P 500 based on Mike’s calls, you would have gone broke. And if you were FIRE, you most certainly would have been heading back to the workforce.

Some Temporary Redemption

Then came 2022, where he correctly called a bear market. The S&P fell 19%, and his view proved right. One correct call out of four years gave him his credibility back. That is how this business works.

It did not last. In 2023 Wilson stuck with a bearish 3,900 target. The S&P finished at 4,769, up 24%. His 2024 target of 4,500 missed the actual close of 5,882 by a whopping 1,382 points, or 31%! Anyone who followed him during those two years and reduced equity exposure or shorted paid a steep price.

To his credit, he turned bullish entering 2025 with a 6,500 year-end target, warned correctly of first-half volatility from Liberation Day tariffs while holding his year-end call, and finished close: the S&P ended 2025 at 6,580, just 80 points shy. A good read.

For 2026 he raised his target to 8,000, around the time the S&P 500 breached 7,500. Let’s hope he is right.

Full record through 2025: 1 nailed, 1 close, five significant bearish misses. Wilson kept his job through all of it and earned millions. He’s got a fantastic gig, and more power to him. But if you are a FIRE investor, you do not have this luxury.

Why Getting the Direction Right Is Everything

The most important lesson I have taken from years of watching Wall Street strategists is this: precision is overrated. Direction is everything.

My favorite Chinese proverb captures it perfectly: if the direction is correct, sooner or later you will get there.

Nobody knows whether the S&P 500 will end in any given year. What you can know, with reasonable conviction built on historical evidence, is the direction of markets over a long enough time horizon. And that directional conviction, paired with appropriate asset allocation, is what separates investors who build wealth from those who lose it trying to time every move.

For 2026, I predicted an up market with a 7,300 year-end S&P 500 target price. With earnings growing far faster than expected, I suspect my target price will end the year light. That said, whether I believe the S&P 500 is going to 7,300 or 8,000, is secondary to whether the direction is correct or not.

The investor who stays roughly right on direction, maintains an age-appropriate asset allocation, and avoids catastrophic mistakes will almost always outperform the investor who tries to call every turn with precision. Not because they are smarter. Because they compound without interruption.

Asset Allocation Is Your Foundation, Not a Secondary Concern

Once you retire early and remove the salary safety net, asset allocation stops being a theoretical exercise and becomes the most practical decision you make.

It determines how much volatility you can absorb without panic-selling, how much income you generate without touching principal, and how long your money can last if markets go sideways for a few years.

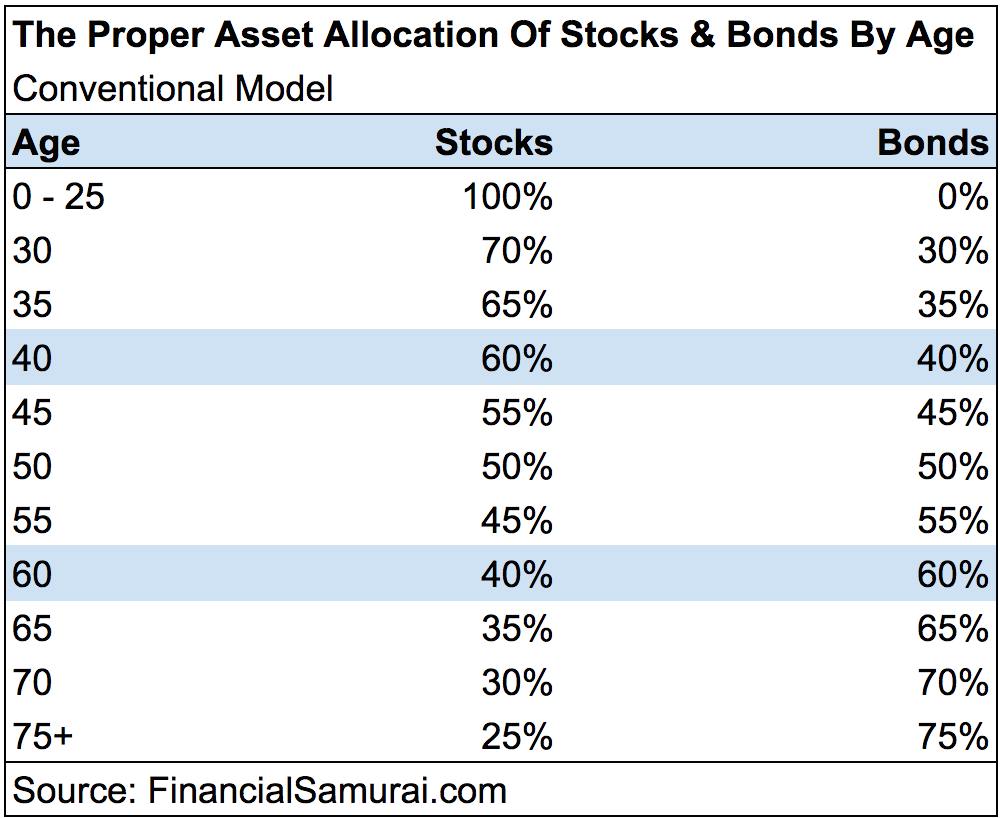

The classic framework is to hold your age in bonds. At 40, hold 40% in bonds. At 60, hold 60%. It is a blunt instrument, but it captures an important truth: as you age, the time you have to recover from a major drawdown shrinks, so stability should gradually take a larger share of your portfolio.

Develop A Diversified Net Worth Beyond Stocks And Bonds

Here are more asset allocation frameworks to consider if the conventional model doesn’t speak to you. In practice, retirees can often hold more in stocks than this rule suggests, for a few reasons.

Social Security, even if it comes later, functions like a bond: a predictable, inflation-adjusted income stream you cannot outlive. A pension, if you have one, works the same way.

Real estate with rental income also behaves like bonds-plus, providing regular cash flow, an inflation hedge, and the possibility of appreciation that fixed income cannot match. If you have two or three of these income anchors in place, your stock allocation can stay higher without exposing you to unacceptable risk.

This is partly why I keep a meaningful chunk of capital in real estate through Fundrise. It gives me bond-like income anchors without the 11pm calls about a broken garbage disposal, which lets me stay directionally invested in stocks without losing sleep. Diversification is key as you age and build more wealth.

The goal is not to hit a precise percentage. The goal is to build a portfolio where a 30% stock market decline does not force you to change your life. Patience is what allows the long-term direction of equities to work in your favor.

Fewer Safety Nets Means More Discipline, Not More Risk

With FIRE, leaving a job to live off your investments is not a finish line. It is a new kind of accountability.

When you are employed, a bad investment year stings but does not threaten your lifestyle. Your salary keeps coming. You can wait.

When you are living off a portfolio, a bad sequence of returns in the first few years of retirement can do lasting damage that a decade of good markets afterward cannot fully repair. Financial planners call this sequence of returns risk, and it is one of the most underappreciated dangers for early retirees.

I can afford to be wrong. I cannot afford to be too wrong. Being wrong means a stock drops 25%, I hold, and I recover. Being too wrong means watching years of savings evaporate in a correction that eventually reverses, but not before it changes my family’s life.

This concern is why any return above the 4% safe withdrawal rate piques my interest. If I can earn 4.5% risk-free in 10-year Treasury bonds, why am I investing in stocks? The honest answer is history. Stocks have compounded at roughly 10% annually over the long run, and giving up that upside entirely feels like leaving too much on the table.

In a bull market, thinking too much about returns relative to a safe withdrawal rate has caused me to be too conservative. For example, I could have invested at least $500,000 more in public venture capital like VCX over the past few years. Alas, I was too satisfied with what I had.

Stay Vigilant With Your Investments

Most people who successfully achieve and maintain financial independence are not the ones who made the cleverest calls. They are the ones who made mostly decent calls, stayed invested through the uncomfortable periods, and never made a mistake big enough to start over.

If you are still building toward financial independence, take calculated risks. Swing for the fences with up to 10% of your investable assets. But once you have reached enough, the goal shifts from maximizing returns to not making a catastrophic mistake. Stay directionally correct, keep your allocation appropriate for your age and income, and let compounding do the rest.

The direction, if you get it right, will eventually take you exactly where you need to go.

Readers, are you a FIRE investor who doesn’t have the luxury of pontificating like Wall Street strategists? If so, has being a FIRE investor made you more conservative than you should have? Or have you become a better investor as a result since so much more is at stake, namely, your livelihood?

The Two Things That Keep Me From Being Too Wrong

The whole point of this post is that a FIRE investor cannot afford to be too wrong, so you build a diversified asset portfolio where one bad year doesn’t change your life. These are the two tools I lean on to do exactly that.

Real estate gives me the income anchors that let me stay invested through the uncomfortable periods. Rental income shows up whether or not the S&P cooperates, which is the kind of stability that keeps you directionally correct instead of panic-selling at the bottom.

If you want that exposure without becoming a landlord, take a look at Fundrise. I’ve invested over six figures across their funds because I want my money working in real estate even when I’m at the beach with my kids. Explore Fundrise here.

And here’s the one mistake no asset allocation can recover from: something happening to you while your family still depends on your income. I can afford to be wrong on a stock. I cannot afford to leave my wife and two kids exposed. That’s the ultimate skin in the game.

Term life insurance is the cheapest peace of mind a FIRE household can buy, and it took me far less time than expected to lock in a policy that fit. Check your rate on Policygenius here.

Read the full article here