Whether you got it from the news, your favorite social media platform, or that one friend who’s a self-proclaimed real estate expert, chances are you’ve heard that mortgage interest rates and home prices are pretty high these days—which is 100% true.

If you’ve been thinking about buying a house or working to save up a down payment, then that news has probably left you with an important question: Should I buy a house now or wait?

To answer that question—and so you can make the best decision for you and your family—let’s look at whether now is a good time for you to buy, or whether you should punt that decision down the road.

Is It a Good Time to Buy a House?

Yes, it is! (Technically.) But really, whether it’s a good time for you to buy a house depends more on your personal finances than on the housing market. Here’s a breakdown of when you should wait to buy a house and when you should pull the trigger:

When to Wait

You should wait to buy a house if you aren’t financially prepared for homeownership. No matter what the housing market is doing, buying a house is a bad idea if you don’t have your ducks in a row.

Specifically, you should wait on buying a house if . . .

- You have existing debt. Focus on paying off all your consumer debt before you buy a house. Getting rid of student loans, credit card payments and car notes will give you more margin in your budget—and that’s super important as a homeowner.

- You don’t have a full emergency fund. Saving up an emergency fund of 3–6 months of your typical expenses before you buy a house will make a broken HVAC unit, fridge or washing machine merely an inconvenience instead of a catastrophe.

- You haven’t saved a strong down payment. If you’re a first-time home buyer, you need a down payment of at least 5–10%. But if you can swing a 20% down payment, that’s even better. Why? Putting 20% down will keep you from having to pay for private mortgage insurance (PMI), an extra monthly fee that could add hundreds to your house payment.

- You can’t afford the house payment. Don’t buy a house if the monthly payment (including principal, interest, taxes, homeowners insurance and HOA fees) on a 15-year fixed-rate mortgage would be more than 25% of your take-home pay. Any more than that, and you run the risk of not having enough money left in your budget each month to put toward other important financial goals—in other words, you’ll be house poor.

We know how badly you want to be a homeowner and to start building equity. But if one or more of those statements apply to you, that’s where you should direct your focus for now. Every day, we talk to folks who bought a house before taking those steps and wound up regretting it because they got stuck with a giant, expensive burden.

We want your home to be a blessing.

When to Buy

If you’ve checked all those boxes, then you’re ready to hire a real estate agent and get to buying! You may be tempted to wait around for a better interest rate or more affordable home prices, but that’s not a good idea for a couple of reasons.

For starters, experts believe home prices will continue to rise for the next two years (at least).1 So if you try to wait to buy until home prices go down, you might be stuck waiting a long time.

Second, if you buy now and interest rates drop later, you can still take advantage of the lower rates by refinancing your mortgage. Think of it this way: You date the interest rate but marry the house.

Overall, you never want to decide whether to buy a house purely based on what the market is doing. If you’re in good shape with your money, there’s no reason to wait.

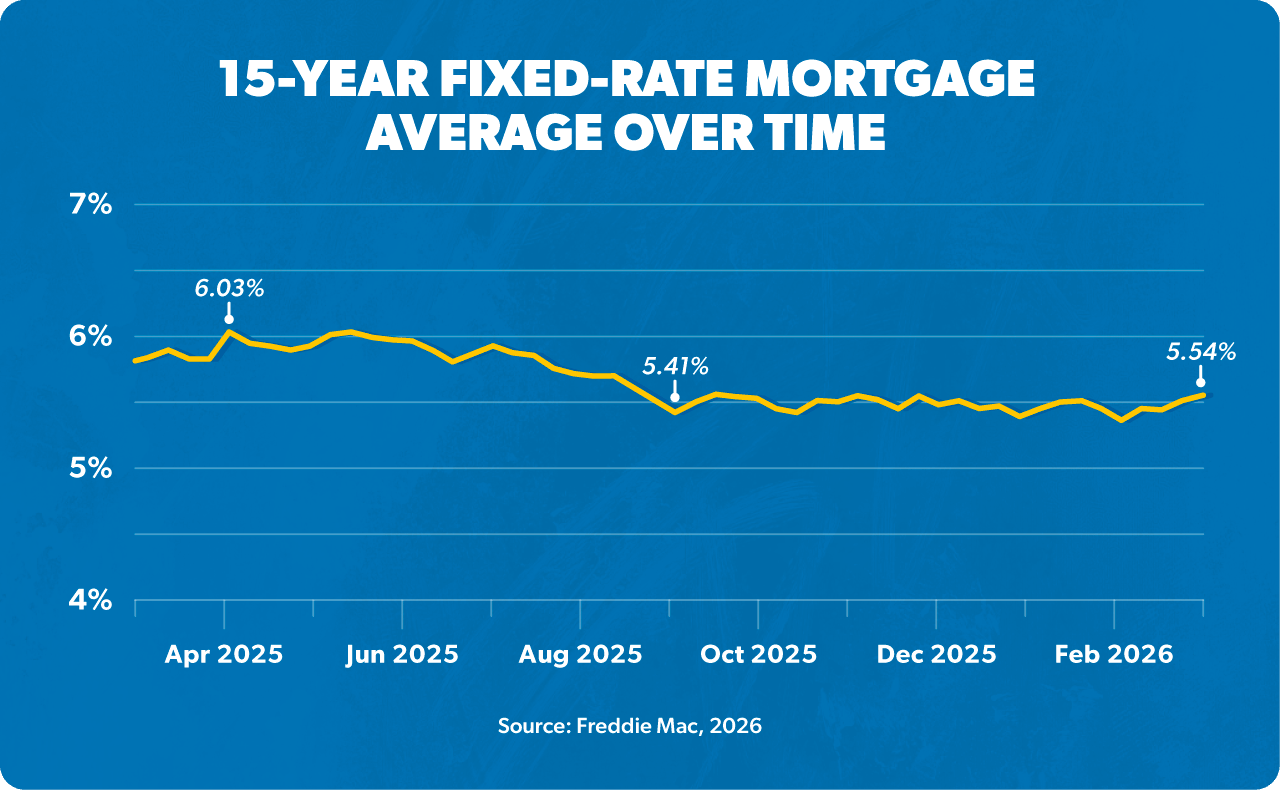

Will Mortgage Rates Go Down in 2026?

Mortgage rates could dip slightly in 2026, but don’t expect a dramatic drop. Why? Because the Federal Reserve (aka the Fed)—the central bank that helps manage inflation and keep the economy stable—is taking a cautious approach as it works to keep inflation under control without slowing the economy too much. And while the Fed doesn’t directly set mortgage rates, it does influence the direction they move.

The Fed currently has the federal funds target rate (the interest rate banks charge each other for overnight loans) set at 3.5–3.75%.2 Their latest projections put the rate at around 3.4% by the end of 2026.3 But keep in mind: 3.4% doesn’t mean mortgage rates will go that low. Mortgage rates are usually 2–3% above the federal funds rate.

Mortgage rates can also move independently of the Fed since lenders are influenced by other factors like the bond market and inflation trends. That’s why no one can predict with 100% accuracy what mortgage rates will do. So be careful not to base your home-buying decision only on rates.

The good news? Rates have come down from the highs we saw in 2023, which is a step in the right direction for buyers.4 But instead of trying to time the market, focus on what you can control—like paying off debt and saving for a strong down payment.

Want to see how a lower rate could benefit your home-buying budget? Try our free Mortgage Calculator.

Why Does the Fed Raise Interest Rates?

The Fed raises interest rates to encourage people to borrow less, spend less and save more—which should slow down inflation. But remember, the Fed doesn’t directly set mortgage rates. They control only the federal funds target rate, which then indirectly influences most other interest rates, including those on loans and mortgages.

The Bottom Line

No one likes high interest rates, but they’re not the end of the world. This is still a great time to buy a house. It’s also a good time to sell a house.

While it’s always great to have a lower interest rate on your mortgage, that doesn’t mean you have to wait years to buy or sell a house—or to refinance if your current loan just isn’t working for you. You get to decide when to buy a house based on what’s right for you and your family—not the Fed.

Read the full article here

")