?")

When Fundrise’s Innovation Fund (VCX) listed on the NYSE on March 19, 2026, its net asset value was $18.97 a share. Within days, retail investors momentarily bid the price above $400. That’s more than 20X NAV, a premium so rich it made 1999 look responsible.

As a shareholder locked up until September 19, 2026, I’ve had a front row seat to the whole spectacle. I wrote about the psychology of that experience in my companion post: What It’s Like To Be A Startup Employee With A 6-Month Lockup.

This post is about the math – calculating VCX’s NAV estimate. Because regardless of what the share price does based on retail sentiment, the NAV provides the base case, fundamental scenario of what the shares are really worth.

Estimating a closed-end venture fund’s NAV takes three basic steps. Let me show you how, so you can run the numbers yourself whenever a new funding round hits the headlines.

VCX NAV Estimate Step 1: Calculate The Dilution-Adjusted Markup For Each Holding

When a company raises at a new valuation, you can’t just divide the new post-money valuation by the old one. New money dilutes existing shareholders, including VCX.

Take Anthropic. At VCX’s $19/share listing NAV, roughly 20% of the fund was in Anthropic at a ~$180 billion valuation. Anthropic then raised $65 billion at a $965 billion post-money valuation. Subtract the new money and the pre-money valuation is $900 billion. So existing shares marked up 5X, not 5.4X. Still a spectacular result, but it’s always good to try and be more precise when real money is at stake.

One piece of vocabulary before we continue, because it trips people up. A 5X markup means the position is now worth five times what it was. In other words, it GREW by 4X its original value. Keep that distinction in mind, because it’s key to Step 2.

Run the same math across the top holdings:

- Anthropic: $180 billion to $900 billion pre-money = 5.0X markup (grew by 4.0X)

- OpenAI: ~$500 billion to $730 billion pre-money after raising $122 billion, with a targeted September IPO above $1 trillion = ~1.5X markup now, ~1.9X by lockup expiration (grew by ~0.9X)

- Anduril: $30.5 billion to $56 billion pre-money after its $5 billion Series H = 1.84X markup (grew by 0.84X)

- Databricks: $134 billion to $175 billion if the rumored round closes = 1.31X markup (grew by 0.31X)

- SpaceX: now public after its June IPO and marked to market daily = ~1.8X markup on the fund’s prior carrying value (grew by ~0.8X)

Thankfully, we can easily input these publicly reported figures into AI to help us make the calculation. However, even still, you need to review the work.

VCX NAV Calculation Step 2: Multiply Each Growth Multiple By Its Portfolio Weight

A 5X markup on a 1% position is a rounding error. A 5X markup on a 20% position is significant. The formula is:

NAV growth contribution = portfolio weight X (markup multiple minus 1)

Why minus 1? Because the original position is already sitting inside the $19 starting NAV. You only add the growth, not the whole new value.

Anthropic’s slice of the fund at listing was 20.5% of $19, or $3.90 per VCX share. After a 5X markup, that slice is worth $19.50. But the fund doesn’t gain $19.50, because it already had the $3.90. The new value created is $19.50 minus $3.90, or $15.60 per share. And $15.60 divided by $19 equals 82%, which is exactly 20.5% X 4.0.

Multiply by 5 instead of 4 and you’d be counting the original stake twice.

Now run the top holdings through the formula:

- Anthropic: 20.5% X 4.0 = +82% to NAV all by itself

- OpenAI with a September IPO: 10% X 0.9 = +9%

- Anduril: 7% X 0.84 = +5.9%

- Databricks: 17.5% X 0.31 = +5.4%

- SpaceX: 5% X 0.8 = +4%

- Rest of the portfolio (Ramp, Canva, and others) at a modest 12% growth: +4.8%

Add up all six contributions and you get 111% total NAV growth, which takes $19 to roughly $40. Anthropic’s 82 points represent nearly 74% of that growth. In other words, of every dollar of new value VCX created since listing, about 74 cents came from one company. This should be both exciting and concerning.

Exciting, because VCX has effectively been a concentrated bet on Anthropic, and so far that bet has paid off spectacularly. Concerning, because if Anthropic stumbles, VCX’s NAV growth will slow or even decline. Concentration cuts both ways.

The optimist’s counter is that the rest of the portfolio has tremendous upside too, and it hasn’t fully shown up in the marks yet. Anduril, for example, is seeing secondary market demand at almost double its latest funding round valuation. If even one or two more holdings go on an Anthropic-like run, today’s garnish becomes tomorrow’s main course.

Step 3: Stack The Contributions In Dollars Per Share

Start at $19 and add it all up.

The math points to a NAV of roughly $40/share right when he VCX lockup expires on September 19, 2026.

Here’s how the estimate evolves across three time frames for 2026 alone. All NAV estimates are based on reported fundraising valuations and expected IPO pricing, not on secondary market activity or where shares might trade after listing.

Today (July 2026): ~$37/share. Anthropic’s Series H closed in late May, so the markup should already be reflected in the fund’s latest marks, along with SpaceX trading publicly.

Lockup expiration (September 19, 2026): ~$40/share. This assumes the Databricks round closes and OpenAI completes its targeted September IPO at around $1 trillion.

Year-end 2026: ~$45/share, with $50 in play. Anthropic has filed confidentially to go public. If it prices anywhere near its last round with even a modest pop, that single position adds another $3 to $4 of NAV because of its concentration.

Of course, the bear case exists too. If AI sentiment cracks before the marks get taken, if Databricks doesn’t close, and if the IPO window slams shut, NAV sits closer to $37. After living through the 2000 dot-com bust from a Wall Street trading desk, I refuse to model only sunshine. Then again, if the IPO window is closed, this makes VCX more valuable.

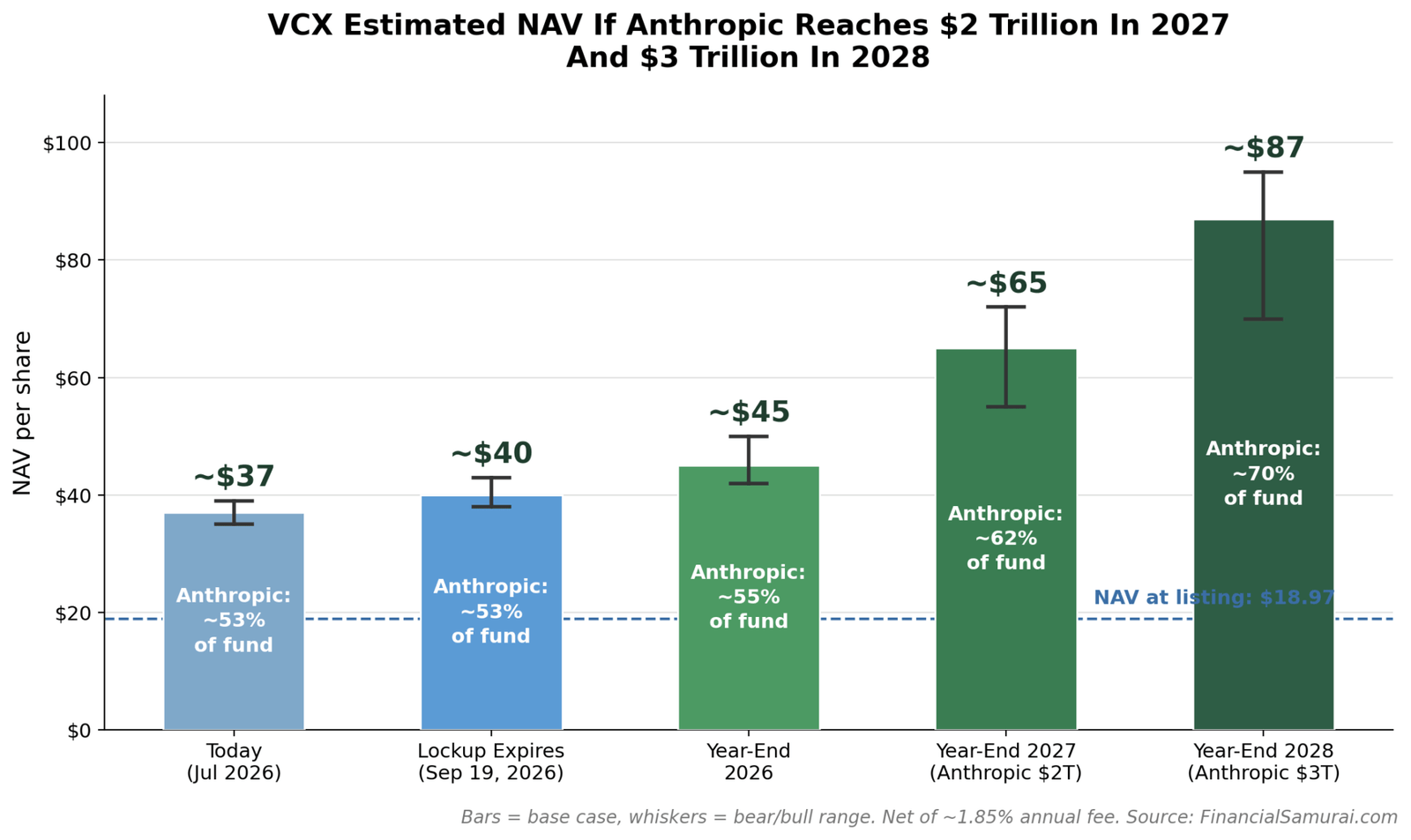

What If Anthropic Becomes A $2 Or $3 Trillion Company?

Now let’s dream a little bigger, because I actually think Anthropic will be strong when it IPOs. The company crossed a $47 billion revenue run-rate earlier this year. In this market, I could see Anthropic becoming a $2 trillion company in 2027 and a $3 trillion company in 2028. Nvidia and Apple have shown the market has no problem paying up for dominant compounders.

Is that my base case? No. A $2 trillion valuation in 2027 implies roughly 40X the current revenue run-rate. But after watching Anthropic go from $180 billion to $965 billion in under a year, I’ve learned not to cap my imagination at what feels reasonable. Anthropic’s revenue could grow to a $100 billion run rate in 2027, make a 20X revenue multiple more reasonable.

Anthropic’s slice of the fund at VCX listing was worth $3.90 per VCX share (20.5% of $19). That $3.90 is the seed that compounds:

- At $965 billion today: $3.90 X 5.0 = $19.50/share. Anthropic alone is now worth more than the entire fund was at listing.

- At $2 trillion in 2027 (~10.5X after dilution): ~$41/share from Anthropic alone

- At $3 trillion in 2028 (~15.7X after dilution): ~$61/share from Anthropic alone

Layer in the rest of the portfolio continuing to compound, with OpenAI public, Databricks marked up, Anduril growing into the defense boom, and SpaceX trading, then subtract the ~1.85% annual management fee, and the estimates look like this:

- End of 2027: ~$60 to $68/share

- End of 2028: ~$80 to $95/share

From an $18.97 listing NAV, that would be a 4-5X in under three years. Without paying a single dollar of premium.

But notice what else happens. At $2 trillion, Anthropic is roughly 62% of the fund. At $3 trillion, about 70%, assuming no growth in the other holdings. Of course, that is unlikely. If Fundrise trims the position to rebalance, the NAV stays the same but the future torque drops. The other positions should continue to grow too.

What This Means For An Investor In VCX

Let’s make it concrete. An investor who put $100,000 into VCX pre-listing owns about 5,260 shares. At NAV alone, with zero premium (or discount):

- Year-end 2026: roughly $237,000

- End of 2027: roughly $342,000

- End of 2028: roughly $460,000

A 4.6-bagger in under three years is a phenomenal outcome by any standard. But notice it’s a long way from the $1+ million some shareholders are dreaming about. That fantasy requires the market to keep paying a fat premium to NAV, which brings me to the most important part of this post.

The Premium Is The Risk, Less So The Portfolio

Here’s the final dose of humility every VCX shareholder needs. The NAV roughly doubling and the share price falling more than 80% from its peak are both true at the same time.

VCX is a closed-end fund. There’s no creation-and-redemption mechanism tethering the price to NAV. Retail investors who paid 20X NAV weren’t buying a portfolio. They were buying a lottery ticket on scarcity, since VCX was one of the only ways the public could own Anthropic, OpenAI, and SpaceX in a single public ticker.

That scarcity is now on a countdown clock. SpaceX is already public. OpenAI is targeting 4Q2026 to IPO. Anthropic has filed confidentially and may list at the end of 2026, or 2027. Every IPO gives investors a way to buy each company directly, so the premium should naturally erode over time, unless VCX continues to invest in the next promising private AI company.

The key word is “over time,” because the sequencing matters enormously. The longer VCX’s holdings stay private, the longer the scarcity premium survives. This is why the Databricks CEO publicly guiding toward a 2027 IPO instead of 2026 is welcome news for shareholders. Databricks is the fund’s second largest holding, and every year it stays private is another year VCX remains one of the only tickets to the show.

Anthropic is the fascinating wildcard. If it IPOs after the September 19 lockup expires, I suspect the premium should continue. An Anthropic debut at ~$1 trillion could get bid up toward $2 trillion given the demand and fundamental growth. That would send VCX’s NAV upward and reignite enthusiasm for the fund at the exact moment shareholders can finally sell.

So when the lockup releases its wave of new supply, the bigger question won’t be what the NAV is. It will be what premium of NAV the market is still willing to pay, and how quickly the IPO calendar dismantles the scarcity that premium is built on.

My math says the NAV keeps climbing. It says nothing about the premium.

Modeling In Mania Is Difficult

Never in my wildest dreams did I think VCX would go up 3X, 5X, 10X, 20X post listing, given I focus on fundamentals. But retail enthusiasm is a variable investors must now consider. We saw it with meme stock mania in 2021, and the Reddit army has only grown since. There is precedent.

Since VCX’s listing in March 2026, hyper AI enthusiasm has cooled, as seen in the share prices of hyperscalers such as Google, Meta, and Microsoft. Microsoft faces more of a long-term structural question, given the fear among software investors that AI will make traditional software irrelevant. As a long-term investor, I view releasing steam as a GOOD thing for sustainability.

The biggest catalyst that could reignite VCX mania is Anthropic going public AFTER VCX’s lockup expires. Sitting here in San Francisco, I’m 90% certain the hype for an Anthropic IPO will be out of control. It may end up the most in-demand IPO in history. In that scenario, demand for VCX should surge along with it.

And there is precedent for how high VCX can fly. It hit $380 in March (higher intraday) and over $250 in May. Meanwhile, Anthropic will likely be more valuable in October 2026 and beyond than it was in the spring, thanks to continued growth. Same retail intensity plus a bigger underlying asset means mania could conceivably bid VCX even higher than before.

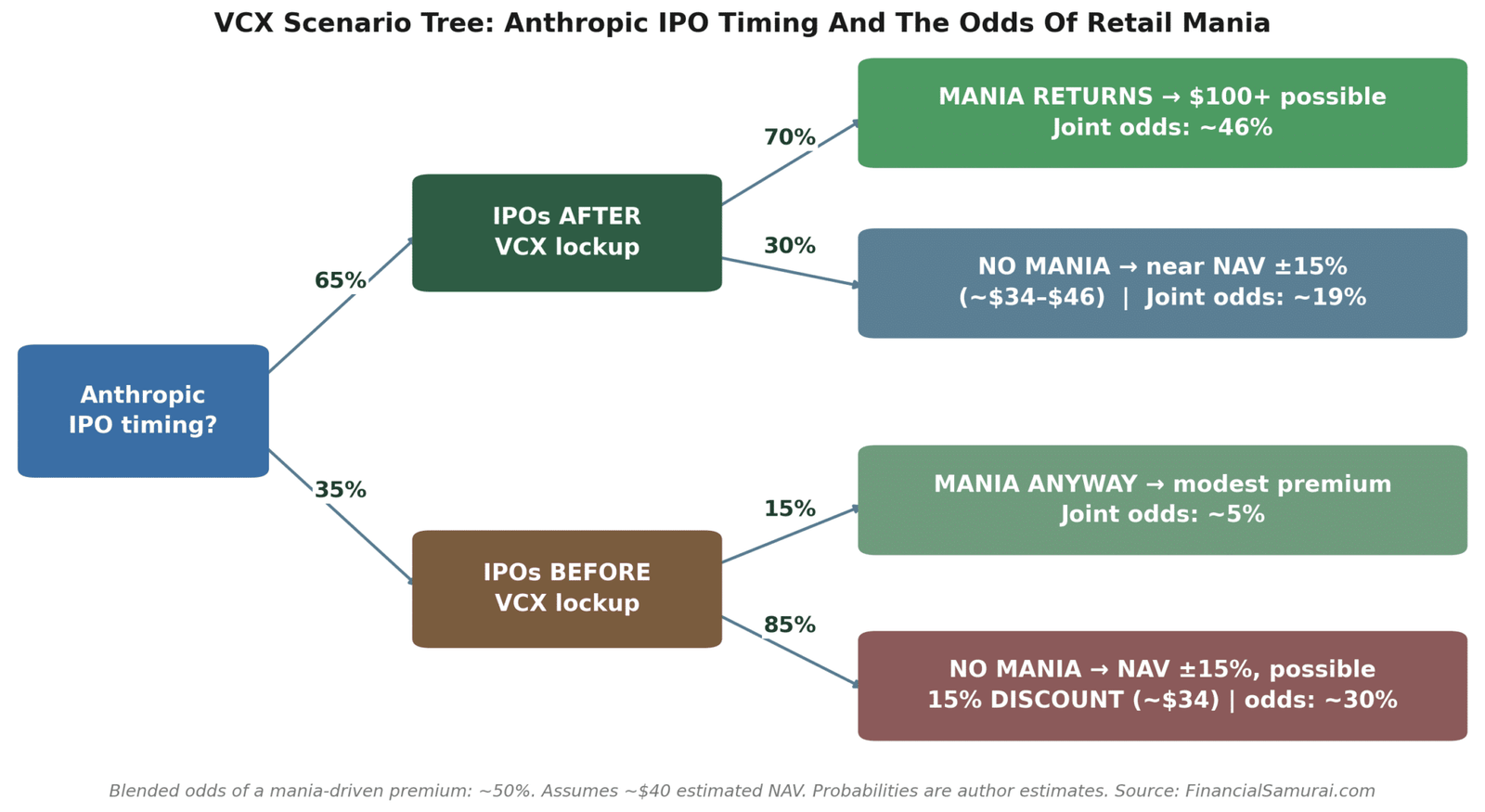

Estimating What Could Happen With Anthropic IPO and VCX NAV

I assign a 65% chance the Anthropic IPO comes after the VCX lockup. If it does, I put the odds of retail mania returning at 70%. If Anthropic lists before the lockup, I assign only a 15% chance of mania, dependent mostly on how well Anthropic trades post listing.

In the no-mania scenarios, I expect VCX to simply trade around its estimated NAV, plus or minus 15%. Blend it all together and I get roughly a 50% chance of another mania-driven premium. A coin flip on fireworks, with a rising NAV as the consolation prize. I’ll take those odds.

Given my shares are locked up anyway, my ideal setup is perverse: VCX dips below my ~$40 estimated NAV, I accumulate more, and THEN the market learns the Anthropic IPO is coming in October or later, reigniting mania and boosting the price to $100+. Buy the fundamentals, get the frenzy for free.

It’s fun to game out upside scenarios with a plan. But whatever happens, I’m happy if VCX simply trades around its estimated NAV. The NAV has grown substantially since listing, and I believe it will keep growing for the next several years. Mania is a bonus. The portfolio is the investment.

Disclaimer and Reader Questions

Before making any investment, please do your own due diligence and only invest what you can afford to lose. Nothing here is specific investment advice for you. This is simply how I’m thinking about my own shares, and our circumstances, financial goals, and time frames are different.

Do you own VCX, and if so, did you buy pre-listing at NAV or post-listing at a premium? What does your own NAV math say, and where do you think the premium settles after the September lockup expiration?

Invest At NAV, Not At A Premium

I just spent an entire section building probability trees to model retail mania. You know what requires zero probability trees? Buying at NAV.

If this post taught you anything, it’s that entry price determines everything. Investors who bought VCX at its ~$19 NAV pre-listing or lower are sitting on a potential double based on fundamentals alone. Investors who paid a 10X premium or greater are hurting despite owning the exact same portfolio. Same Anthropic, same OpenAI, wildly different outcomes. The only variable was the price they paid to get in.

Fundrise has reportedly filed to launch VCX 2, though the timing and final structure remain uncertain. If a sequel launches, the window that matters is the pre-listing one, where you buy at NAV like the first VCX’s biggest winners did. Existing Fundrise investors will be notified first, and you can open an account here to get on the list. Free to sign up, and it beats setting a price alert and praying.

In the meantime, every fund on Fundrise’s platform, from private real estate to private credit, transacts at NAV. No premium to overpay, no lockup-expiration supply waves, no mania variable to handicap. The entire second half of this post, all the premium modeling and probability trees, simply doesn’t apply. You get the fundamentals without the frenzy. Same three-step logic, applied to buildings and credit instead of AI unicorns.

Disclosure: Fundrise is a long-time sponsor of Financial Samurai, and I am an investor in Fundrise funds, including the Innovation Fund (VCX). All NAV figures in this post are my own estimates based on publicly reported funding rounds, not Fundrise’s official marks. This is not investment advice.

Read the full article here

?")