I’ve spent 45 years as a personal finance expert and author— and if I had to point to a single category where smart, financially literate people leave the most money on the table without realizing it, I’d point straight at auto and home insurance.

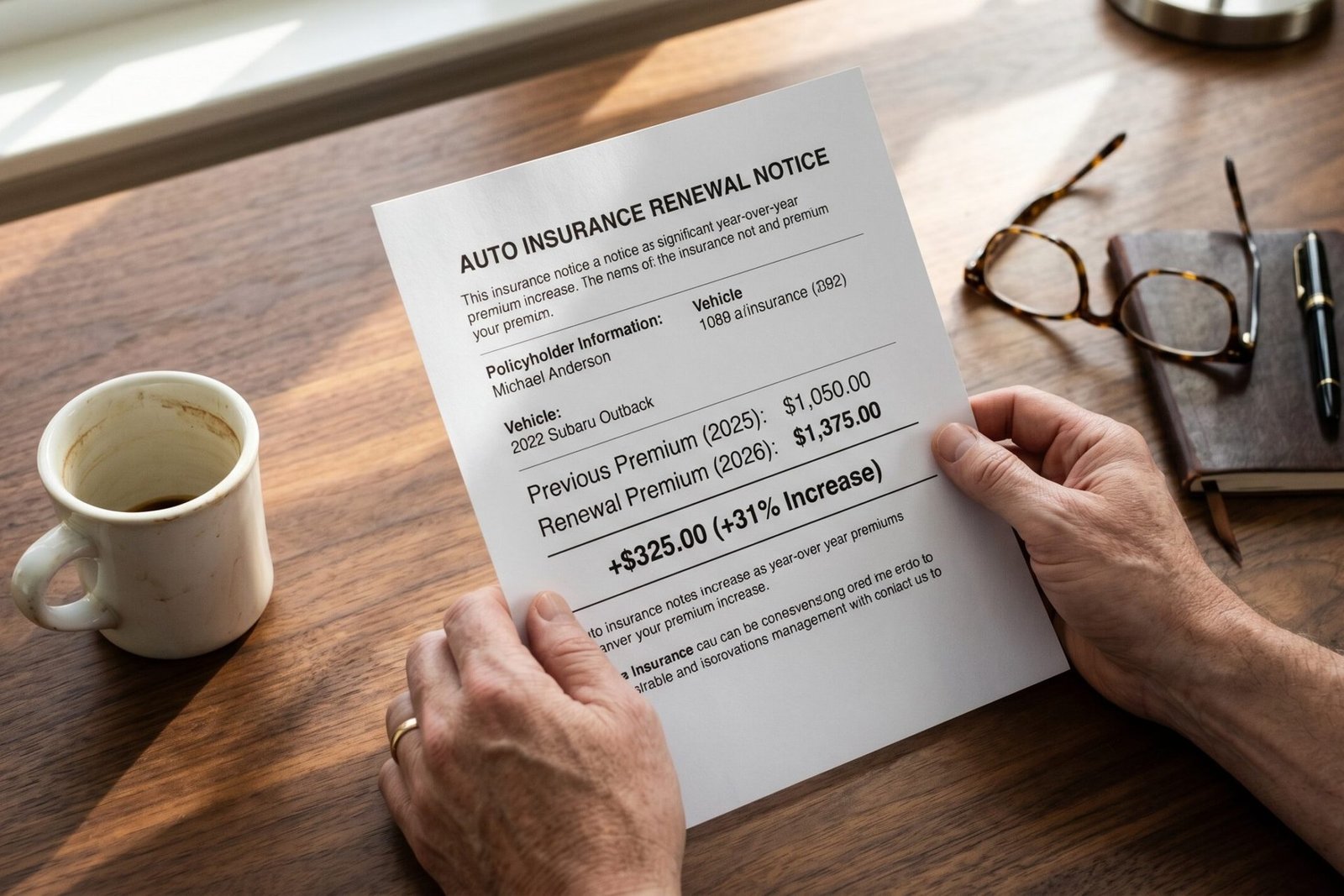

The reason isn’t laziness. It’s an industry practice with a name most consumers have never heard of: price walking. It’s legal in nearly every U.S. state, every major carrier runs some version of it, and it’s quietly costing loyal customers anywhere from $400 to $1,100 a year on auto coverage alone.

If your auto and home policies have renewed automatically for two or more years without you comparing quotes, the math says you’re almost certainly overpaying. Here’s how it actually works, why right now is a particularly costly time to ignore it, and what to do about it in roughly the time it takes to finish a cup of coffee.

Already know you want to check? There are plenty of places to do it, including with a partner we’re currently working with:

Compare your car and home rates against 50+ carriers free — about 5 minutes, no commitment, no spam calls.

The Industry Term Most Consumers Have Never Heard Of

Price walking is the practice of charging existing customers more for identical coverage than carriers charge new customers with the same risk profile. The longer you stay, the higher your “loyalty premium” climbs — typically a few percent at each renewal, year after year, until the gap between your rate and a new customer’s rate is hundreds of dollars wide.

This isn’t conspiracy thinking. The UK formally banned the practice in 2022 after their Financial Conduct Authority concluded loyal customers were being systematically overcharged. In the U.S., a handful of states have started restricting it, but in most of the country it remains entirely legal and entirely standard.

The result for the typical long-tenured customer: $400 to $700 a year overpaid on auto coverage compared to a new customer with an identical profile. Add stale information your insurer never asks you to update — fewer commute miles since you moved, a paid-off vehicle, a home security system — and the gap can widen to $1,100 a year or more.

The same is true for home insurance.

The 10-minute fix: Comparing car and home quotes through Insurify doesn’t require switching, doesn’t trigger a hard credit pull, and doesn’t unleash spam calls. It shows you, side by side, what 50+ top carriers would charge a new customer with your profile right now. If your current carrier is competitive, you’ll know. If they’re not, you’ll be holding $400 to $1,100 a year worth of negotiating leverage.

Either way, you win; either by finding a lower rate, and knowing you’re already getting the best deal.

Why the Window Is Unusually Open Right Now

For three years following the pandemic, auto insurers raised rates aggressively to cover repair-cost inflation, supply-chain delays, and a spike in accident severity. Many of those increases were genuinely necessary. But the cycle has turned — in 2026, carriers are sitting on healthier reserves than they’ve held in years, and several majors are competing hard for new market share.

That competition shows up in one specific place: the rates carriers offer to new customers. Headline new-customer rates are aggressively low right now, while existing-customer rates are still carrying the post-pandemic correction. That gap is the price-walking gap, and it’s wider today than it’s been in a long time.

Soft windows like this one tend to close without announcement. A 10-minute car and home insurance comparison locks in the math while it’s still in your favor.

The Bundling Mistake That Costs Homeowners Twice

If you own your home and your auto and home policies are with two different carriers, you’re almost certainly leaving money on the table a second time. Carriers that write both lines typically discount each policy by 10% to 25% when you bundle — combined annual savings of $400 to $800 are common, and often achievable in a single transaction.

This matters more than usual in 2026 because home insurance has been the more painful side of the equation. Home insurance premiums are up roughly 21% over the last three years, driven by climate-related claims, rebuilding-cost inflation, and several major carriers exiting high-risk states entirely. The bundle discount is one of the few clean offsets to that trend that’s still available without changing your coverage.

What the Industry Won’t Tell You at Renewal

Two specific savings categories almost never surface at renewal time, even though they apply to a huge share of policyholders:

Low-mileage discounts. If you’ve shifted to remote or hybrid work since 2020 and your annual mileage has dropped meaningfully, you may qualify for 15% to 30% off your auto premium. Your insurer is not going to call you to tell you that.

Newer telematics and safe-driver programs. The discount programs offered to new customers today are materially better than the ones available five years ago. Existing customers are typically left on legacy programs unless they specifically ask — or unless they get fresh quotes that price the new discounts in automatically.

There are also discounts available for home insurance, from smoke and burglar alarms to a new roof and security cameras. Even your age could get you a discount, as could not having filed a claim in years.

These potential discounts surface naturally when you compare quotes through a marketplace, because the marketplace asks you the same questions a new-customer application would. Your renewal notice doesn’t ask any of them.

Compare your real rate against 50+ top carriers in 10 minutes.

No spam calls. No commitment. No catch. Over 10 million Americans have used Insurify, which holds a 4.7-star rating on Trustpilot. Customers who switched in 2026 are saving an average of $1,100 a year on auto coverage.

The Bottom Line

The financial pressures hitting American households in 2026 — sticky inflation, AI-driven layoff anxiety, elevated housing costs — are mostly outside any individual’s control. Insurance is the rare exception. It’s a four-figure annual line item that responds directly to ten minutes of effort, and the people I’ve watched build real long-term net worth treat it that way.

What those people understand is that “loyal customer” is not a status the insurance industry rewards. In most states, it’s a status the industry quietly charges a premium for. The fix isn’t dramatic — it’s a 10-minute side-by-side comparison that either confirms you’re paying a fair rate or hands you $500 to $1,100 a year you didn’t know was there.

If you haven’t compared auto and home quotes in the last two years, the math is heavily on your side, and there’s no scenario where checking costs you anything.

Compare your auto and home quotes at Insurify: free, 10 minutes, no spam calls → 50+ top carriers · Over 10 million users · ⭐ 4.7 on Trustpilot

MoneyTalksNews is an independent personal finance publisher. We may earn a referral fee from partner services at no cost to you. Our editorial recommendations are based on merit, not compensation.

Read the full article here