Recently, a home in the beautiful Forest Hill neighborhood of San Francisco was listed for $2.4 million. It had four bedrooms, three bathrooms, and a modest 2,250 square feet. The home had been remodeled about 15 years earlier and was squarely in the price frenzy zone.

As we do with every open house, my wife and I made bets on what we thought the house would sell for. She guessed $2.65 million, and I guessed $2.75 million. $350,000 over asking to $1,200/sqft seemed reasonable given all the foot traffic and its bay view from the top bedroom. However, there was no usable front or back yard and there were a couple of quirks.

No matter. A month later, we found out the home sold for a whopping $3.5 million! At first, I felt fantastic. Given that we own a home on the west side too, we immediately felt wealthier. However, once the feel-good effect from the sale faded, I started feeling a little disappointed.

The Disappointment Of Selling A Home In a Rising Market

The worst scenario for a homebuyer is buying a property at the top of the market and then watching comparable homes sell for lower prices over the next several years.

The good thing is you have to be extremely unlucky to top tick the housing market. And given most people live in their homes for an average 13 years, you should be able to ride out the cycle even if you buy at the top. Housing downturns usually do not last more than five years, and often only last two to three years.

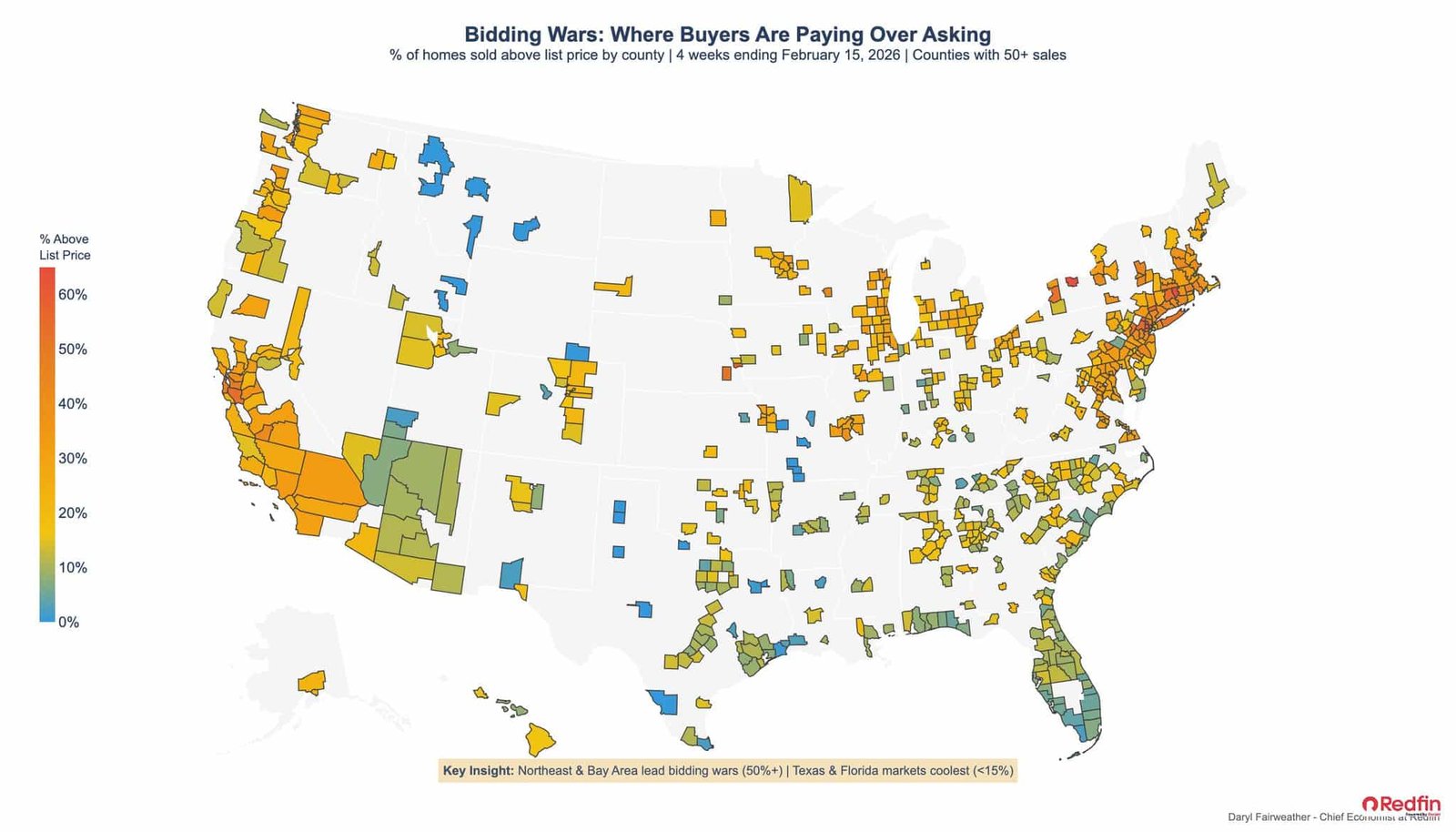

The second worst home transaction is selling a home and then watching comparable homes, and worse, inferior homes, sell for higher prices than your home. As one year has passed since I sold my previous primary residence in the first quarter of 2025, I am now experiencing this growing regret based on all the bidding wars I’m seeing.

Perhaps you will experience this psychologically bummer as well, which is worth talking about. You might even start making excuses, like I am about to, to justify your suboptimal selling decision.

Why I Sold My Home Even Though I Felt Prices Would Continue To Increase

I did not need to sell my home that I bought during the lockdowns in 2020. I could have kept renting it out and dealing with the maintenance and tenant issues.

However, even though I was bullish about the San Francisco housing market due to chronic undersupply and the boom in artificial intelligence, I decided to sell the house after one year of renting anyway.

Here was my thought process behind selling a home I did not need to sell, which may help you decide what to do with your house in a rising property market.

1. Too Old And Tired To Deal With So Many Rental Properties

Making a fortune in real estate is all about a war of attrition – kind of like what’s happening in Iran right now. Those who can hold out the longest tend to gain the most. Unfortunately for me, I was stretched thin managing four rental properties in San Francisco plus a Lake Tahoe vacation rental, which is outsourced.

I did not want to sell the property when it became available to rent at the end of 2023 because I was bullish on the San Francisco Bay Area housing market. Therefore, I decided to suck it up and find tenants to buy myself at least a year of appreciation. If the tenants stayed longer than a year, then great.

I put in the work tidying up the property and marketing it, but unfortunately, the best I could do was find four roommates who had a cat and did not have much experience taking care of a property. They were all in their mid-20s and working in technology, except one who was getting a PhD.

They were not bad tenants, but they seemed a little irreverent about taking care of my property. The yard became overgrown and they dinged the side walls in the driveway. Inside, they yanked my kitchen faucet nozzle right off, causing water to leak everywhere. Instead of admitting they broke it, they just said it started leaking.

I didn’t put up a fight. Instead, I ended up buying a new faucet for about $380 and getting my guy to fix it for another $100.

Winter Storms Can Be Damaging

After the heavy rains in the winter of 2023 and 2024, I also did not want to deal with any potential leaks or downed trees in the yard for one more year. My downhill neighbor had asked me years ago to cut down a tree on the hill that could fall into their backyard. So I hired tree trimmers and spent about $600 to top the tree and lighten the load as a good neighbor.

In addition, I had already spent time fixing some west facing windowsill leaks from the outside, which was disclosed. I did not want to deal with potentially fixing those leaks again and then possibly facing roof issues too.

So after a year of renting the place, my tenants decided they wanted to move out. I felt like this was destiny telling me to sell.

2. Overleveraged And Outside My Risk Tolerance

I have been a San Francisco landlord since 2005. During this time, I have experienced plenty of headaches. As a result, I decided the maximum number of rental properties I could comfortably manage myself was three in the city.

I did not want to hire a property manager because I do not have a day job and I know a lot of handymen from all my remodeling projects. I can maintain properties myself without paying a property manager a month’s worth of rent rent as a fee.

However, I decided to swing for the fences in late 2023 and bought a dream property on a large lot with a view of the Golden Gate Bridge. It had originally been on the market in 2022, and I desperately wanted to buy it. But I did not have enough money at the time, so after a long period of consideration, I let it go.

Then the listing agent contacted me again the next summer and said they would try again at a lower price. I was intrigued because my stocks had rebounded, and so had my cash position due to continued savings.

Ultimately, I bought this property and rented out my old house. But the problem was now I was managing four rental properties in the city, which was one rental property above my comfort zone.

So I was essentially rolling the dice that nothing bad would happen for at least one year.

The Southern California Fires Were A Catalyst To Sell

When the terrible fires in Southern California ripped through Pacific Palisades and destroyed multiple neighborhoods overnight in January 2025, I decided I did not want to test fate any longer. These multimillion dollar homes just disappeared overnight.

Reports also said State Farm had backed out of many homeowners insurance policies months earlier. So conceivably, some homeowners lost millions and did not have insurance to rebuild.

The fires reminded me of 2008 and 2009, when I lost ~40 percent of my net worth that took 10 years to build. Meanwhile, some colleagues lost everything because they used margin and had poor asset allocation and risk management.

As a father to a five year old and seven year old at the time, I was busier than ever. Wanting to spend more time taking care of my son is the number one reason I sold my other primary residence in 2017 that turned into a rental for three years prior.

Couple that with the launch of Millionaire Milestones in May 2025, and I simply wanted to reduce risk exposure and focus more on my craft.

Note: If you’d like to get a signed copy of my USA Today bestseller, check out my free Empower financial review post for instructions. Getting a professional to review your investments is helpful in building greater risk-appropriate wealth over time.

3. Happy To Pay Down Debt

The easiest way to pay down mortgage debt is to sell a home with a mortgage, not pay down bits and pieces of principal whenever you have extra cash flow. Although the interest rate was only 2.5 percent, the mortgage amount was still about $1.4 million. The 7/1 ARM was also expiring in 2027, so at least I got a good five years of an ultra-low rate.

The rental income of $9,000 was nice, but after paying the mortgage and property taxes, it got whittled down to about $3,500 a month. At least by paying the mortgage, I was also paying down about $2,500 a month in principal.

But the $3,500 a month in cash flow, or roughly $6,000 a month in net worth growth, was not worth the risk of owning the property or the pain of maintaining it.

The older I get, the more I want to pay down debt and minimize volatility. The triple benefit to paying off a mortgage early with guaranteed returns, increased cash flow, and greater courage are wonderful.

4. Would Only Sell If I Hit My Aspirational Target Price

Given I was bullish on the San Francisco housing market, I set a realistic but aspirational sales price for my home. I told my agent that if we did not hit that price, I would not sell the home. Expectations were set.

This is how I helped ensure I would be satisfied with the sale and reduce my chances of seller’s remorse.

Ultimately, I got a preemptive all cash offer with a 10 day close. The price exceeded my aspirational sales price by $18,000 after a couple rounds of counteroffers. So I took it.

I was hoping to get a crazy price that was $100,000 higher than my aspirational price, but another bidder was nowhere to be found. This was despite pinging the Top Agents Network list multiple times over two weeks.

5. Had A Clear Plan For Reinvesting The Home Sale Proceeds

After simplifying life with one less mortgage and one less financial account to deal with, I came up with a framework for how to reinvest the proceeds. My plan was to attempt to make a 10% return.

Because I was bullish on technology and 4 percent plus yielding Treasury bonds, I decided these were the two areas I would invest in over the next six months. I initially allocated about 70 percent of the home sale proceeds to the S&P 500 and individual tech names, mostly Google and Apple. Then I bought individual Treasury bills and Treasury bonds yielding between 4 percent and 5 percent.

I did not time the investments correctly because I started in March 2025, about a month before Liberation Day, when the markets tanked by up to 20 percent. Please be careful buying the dip too often and too soon as we head into another correction. But I did keep investing through that period, and the markets ultimately recovered to where they are today.

In addition, during the summer, I decided to invest $191,000 of cash and maturing Treasury bills into Fundrise’s venture product, which ended up rising by 43.5% for the year. I had a realization that if I was willing to invest $250,000 in each child’s 529 plan, then I should have the confidence to invest a similar amount in the very technology that may make life more difficult for my children.

So far, the home sale proceeds have exceeded my 10% target return. However, without a proper asset allocation, I could easily give up a lot, if not all, of the gains in the coming year.

6. Tax Free Exclusion Amount Was There To Take

By renting out the property for only one year and living in it for four of the past five years, I was able to take full advantage of the $500,000 tax-free capital gains exclusion for married couples.

If I had found another tenant in 2025, there was likely a 75% chance they would stay longer than one year, especially if they were a family. The longer I rented out the property, the greater the risk of falling outside the “two out of the last five years” ownership-and-use test required to qualify for the full exclusion.

In addition, any non-qualified use (periods when the property is rented after 2008 and not used as a primary residence) would begin to reduce the eligible tax-free exclusion on a prorated basis once the property no longer satisfied the two-out-of-five-year rule.

7. Still Have Exposure To San Francisco Real Estate

Finally, I told myself that even if west side home prices continued to appreciate after selling, I still owned properties in the area that would continue to appreciate as well. I just wouldn’t make as much from my real estate holdings.

If this had been my only rental property, I would not have sold.

You Cannot Get The Timing Right Every Time

In retrospect, I wish my tenants would have given their notice at the end of 2025 instead of at the end of 2024. One more year of property appreciation of 5% – 10% would have been nice. It was a great home for a family of four or five making the typical dual income tech household income after 10-15 years of experience.

It was priced slightly above the frenzy zone, which provided relatively good value. But I felt that in time, the frenzy zone would expand to include this property as well.

But I also forget how much more stress I would have had maintaining this property, especially if it had a leak, a tree fell on it, or a tenant started a fire. In fact, I drove by the property one day and saw roofers replacing a portion of the roof. So maybe something happened. I am not sure.

Today, my asset allocation is closer to my desired 35 percent in public stocks, 40 percent in physical real estate, and the rest in venture capital, bonds, cash, and private company equity. As a result, I feel more at peace that no matter what happens, everything will be manageable and fixable.

It also feels great not to have to pay over $30,000 a year in property taxes for this one home alone. I wish there was less corruption and more efficiency in the San Francisco government. Thankfully, conditions seem to be improving with our new mayor.

Extremely Grateful For The Property

This was a wonderful remodeled house that took great care of us for three and a half years during the heart of the pandemic. It gave us more space when we needed it most. Our daughter was born eight months before we moved in, and our home at the time was going through a heavily delayed downstairs remodel.

I will be forever grateful for its service. Come to think of it, I would have been fine selling the property for the same price I purchased it for, which would have resulted in about a 5 percent loss after all fees, transfer taxes, and fixes. The house saved us during one of the most trying times, especially with a three year old and a newborn.

So instead of viewing the house sale purely as an investment that could have made us even more money, I now view it as a solid lifestyle investment during a tough time. It just happened to have also made us some money.

More Passive Investments Over Time

There has been over three years of underbuilding or no building in many parts of the country. Supply will start getting absorbed, and there should be rental pressure across the nation going forward. I am already seeing 10 percent rent increases here in San Francisco.

The older I get, the more I want to simplify life. I am happy to reinvest my rental property proceeds into 100 percent passive investments like stocks, bonds, and private commercial real estate. My kids are almost halfway out of the house, and I do not want to spend any more time than necessary managing rentals.

Readers, have you gone through an experience where you sold a property and the market kept going up, up, and up? Did you believe prices would continue to rise after selling? How did you handle the situation and still benefit?

Get my posts in your inbox as soon as they are published by signing up here, and subscribing to my free weekly newsletter here. I’ve been writing about personal finance since 2009, and everything is based off firsthand experience and expertise.

Read the full article here